Aug 13 2020 - YRC Worldwide Inc.: Shares Still Heavily Discounted - Part1B

SIX: Network optimization efforts will maximize load factor across the company’s network, leading to increased operational efficiency, density, yield, and incremental operating ratio improvement.

Some investors seem to think that YRCW's network is somehow working against the business, and that's a wrong way to look at it. Most businesses are generally always looking for ways to improve the way they operate. Over the last year and a half, management has taken steps to improve its network and reallocate business value by eliminating duplicate service facilities across the network, and redesigning line haul operations to help build network density.

The company’s engineers are also improving line-haul operations in close regional segments to increase the availability of next-day service offerings. These services reduce the number of stops required and the probability of damaged freight due to less freight handling. Most importantly, next-day services support higher margin business which translates to additional free cash flow.

These actions are different from having to downsize the company following the 2007-2008 financial crisis. This optimization program is not a capital-raising effort to cover debt or interest expenses, and certainly not an effort to resize the business due to a collapse in demand. Instead, this program was specifically designed to build load density across the network. Density is something other LTL carriers have had for the last 10 years, and it's why they have been so profitable. For supporting evidence, here is a recent quote from Gregg Grant, Old Dominion's CEO:"...we can continue to drive this operating ratio lower once the density factors come back, but it's the density and the yield and both of those generally require a positive economic backdrop to support each."

During the 2018 peak LTL freight environment, YRCW was at less than 30% into their fleet replenishment program, and still developing their network strategy. As a result, the company was unable to fully capitalize on that market like competitors did. The company’s disappointing financial performance during in that season led to analysts’ downgrades, and sent the stock plummeting back down to single digits.

Today, the process is nearly complete, as the network was down to 335 facilities at the end of the second quarter from 351 at the beginning of the year. According to CEO Darren Hawkins, the process should be completed by the end of the year with the final service facility count down to 325.

In the process of improving freight flows across the network, management is looking for cost savings from redundant buildings leases and selling underutilized property they own. Some proceeds may go towards paying down debt, other times towards new equipment or technology. Management is always transparent on how proceeds will be distributed.

Source: YRC Worldwide, Inc.

In Centaur's view, the company's objective seems pretty clear, they're looking towards the next economic boom, and they're positioning the company to take advantage of it. When that time comes, the tables will turn. With the company in the right position to capitalize on higher volumes, profit growth, analyst upgrades, and renewed institutional investor interest are sure to follow.

SEVEN: Software migration to the cloud will deliver efficiency gains and support pricing through improved business visualization, leading to further operating ratio improvement.

Adding to the benefits of having a new fleet and more efficient network operations, cloud-based software is critical to extracting additional value from the business. As discussed in this Forbes article, the company managed to eke out enough operating cash to pay down about 60% of its long-term debt and still reinvest back into the business despite relying on multiple legacy on-premises software packages.

The company-wide transportation management and enterprise resource planning software roll-out over the last year has temporarily added costs, but should dramatically improve visibility over the business. Going from legacy to real-time data should allow management and engineers to pinpoint exactly which areas of the network need further improvement, and examine how productive the workforce is.

At the same time, the mountains of real-time data may help the company properly bill customers for driver delays and freight discrepancies, while providing leverage for negotiating better contract rates.

The notion here is real-time cloud-based-data will build onto the other operational areas discussed, and inevitably translate into lower operating expenses, operating ratio improvement, profit growth, and high returns for shareholders. Lastly, all the incremental returns from modernizing the business will have a greater impact on YRCW’s bottom line, than the efforts prime competitors are undertaking to improve on their all-time low operating ratios.

EIGHT: Labor management synergies gained in the 2019 collective bargaining agreement will partially offset wage inflation, healthcare, welfare, and overtime costs.

Labor management has historically been an area where YRC executives had relatively little control compared to competitors. Old Dominion is a great example of this divergence in labor costs. Naturally, figuring out what ODFL does right helps to pinpoint where YRCW does not do as well. It seems as though every ODFL earnings call Q&A is filled with analysts trying to figure out what makes ODFL so efficient and what the company’s operating ratio will look like several quarters down the road. During the Q1 2020 conference call, Old Dominion’s CFO, Adam Satterfield perfectly described the advantage LTL competitors have had over YRCW in the past, as he addressed an analyst question about variable costs. Satterfield said:

“Over time, the operating ratio level that we've improved, most of the improvement has come in those direct operating costs, which most of which are variable. So, we've got an improvement over the years, and our overhead costs have stayed relatively consistent as a percent of revenue. But we've always, in our history, tried to work on operating efficiencies, and we have a continuous improvement process that focuses on quality and we've always made efforts through technology improvements and just general process improvement to try to optimize mainly labor cost as a percent of revenue. And so that's just that's been a focus. It will continue to be a focus.”

The key words to focus on from this quote above are: “optimize labor cost as a percent of revenue.” YRCW’s labor cost challenges can be directly linked to their previous collective bargaining agreement with the Teamsters. In the labor agreement ratified last year, the company new gained language which allows management more control over labor utilization.

Specifically, management can now hire non-CDL employees at lower wages and increase usage of purchased transportation. In our research, we noticed that most non-union LTL carriers have strict limitations on overtime hours and overtime pay per hour. Most of YRC’s competitors pay their workers the same regular rate per hour for each overtime hour worked. Better yet, most of YRC’s LTL competitors are so well-staffed, they do not allow workers to put in overtime hours at all.

This contrasts with YRCW’s labor policies. YRCW pays it workers regular pay plus half, and in certain cases up to double and triple their regular hourly pay for overtime when holiday or weekend work is required. With an optimal network in place, a modern fleet, cloud-based software, real-time data, increased purchase transportation budget, and labor flexibility, the only missing ingredient is a larger headcount of experienced and well-trained employees.

This is not something easily or quickly accomplished, but contrary to popular misconceptions about unionized LTL, labor costs can certainly be brought down closer to the industry average. Centaur Investments believes these synergies will lower YRCW's labor cost as a percent of revenue, and result in tens of millions of dollars in reduced operating expenses per year. These savings should further contribute to net income growth and high returns for shareholders. Point number nine below, builds on to the synergies gained in the labor agreement.

NINE: Workforce consolidation, training, and organizational culture development will improve worker morale, productivity per labor hour, and further reduce overtime costs.

Another area where the company has opportunity for improvement is in its workforce. The intuition here is that workforce consolidation in combination with cloud-based resource planning will facilitate recruiting, hiring, training, and creation of new sales opportunities for the company.

Last year, the company trimmed dozens of corporate-level executive positions, and shuttered their New Penn headquarters, transferring most of those office operations to their Kansas-based headquarters. They also consolidated their entire sales force which operated independently at each of YRCW’s regional companies. After consolidation, the sales workforce is now cross-selling all five regional brand company services to customers across North America.

Centaur Investments views these changes as efforts by YRCW's executive leadership and board to streamline the entire business' organizational structure. We believe management will continue to work their way from the top of the company's organization chart down to the service facility operating levels. In doing so, they will effectively eliminate 'bad apples' from the business, onboard more engaged lower-level and middle-level managers, and motivate the rest of the workforce to improve performance.

In thesis point seven, we linked to a Forbes article about all the cloud-based enterprise resource planning software YRCW has been rolling out company-wide. The software will allow managers to keep track of employee productivity and provide essential data for performance evaluations and training. As an example of the power of these tools, managers at service facilities can break out individual productivity data with dock workers and pickup and delivery drivers and incentivize them to increase individual productivity by holding each other accountable.

These are solutions that competitors already have in place, but YRCW can still tap into to improve culture, labor utilization, and labor cost per revenue. While competitors will mostly maintain their top-level performance, YRC can potentially experience substantial operational efficiency gains from these new labor resources. For investors who think culture development is impossible at a unionized LTL carrier, YRC’s unionized LTL peers at ArcBest Corp., FedEx, UPS, and XPO Logistics are perfect examples that it is certainly possible. Keep in mind that unionized LTL peers do not have taxpayer ownership to think about.

Source: Slide 6 from YRC Worldwide's June 2019 Presentation

Source: Slide 6 from YRC Worldwide's June 2019 Presentation

Finally, investors must understand that YRCW’s distressed condition discouraged high skilled and experienced workers from making YRCW their first choice of employment. The company’s older than industry average fleet equipment also played a role in deterring experienced applicants.

Still, nothing was more challenging than having to recruit drivers and dock workers as the U.S. unemployment rate hovered near all-time low in recent years. The low unemployment rate meant YRCW had to compete in a shrinking labor pool of skilled workers, while many of candidates potentially considered YRC their last choice. When the LTL market heated up in 2018, the entire industry was hiring whoever they could from that shrinking labor pool and training them on the fly.

Things could not more different today. The national unemployment rate is over 10%, and employment is down across the industry due to lower demand and capacity requirements. The new equipment and technology the company is introducing may help the company attract higher skilled workers, as well as lower and middle-level management. Centaur Investments believes that as YRCW's operations improve their reputation will also improve. With an improved image and generous health and welfare benefits guaranteed by collective bargaining agreements, YRCW could quickly go from being an experienced job seeker’s last choice to their first.

TEN: Apollo term loan covenant amendment and 2020 CARES Act loan package allows management to focus on their multi-year strategy and clears the runway to sustainable profitability.

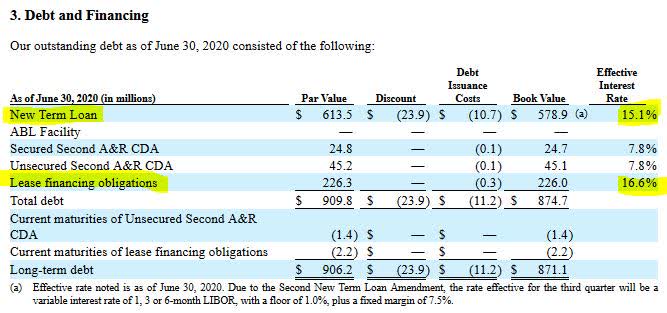

On April 8, the company filed an 8-K with the SEC announcing they had amended the debt covenant on their 0 million term loan which they refinanced last year through Apollo Global Management, Inc. (APO). In order to manage liquidity during the government-mandated lockdown period, the company requested a six-month window to allow for payment-in-kind interest payments, and a temporary waiver on the 0 million minimum adjusted EBITDA requirement through the end of the year. While the creditor agreed to work with the company through the pandemic, they imposed a high interest rate penalty which led to a 510 basis point increase in effective interest over the original terms. The company's most recent 10-Q filing shows the effective interest rate on the term loan was 15.1% at Q2-end 2020 versus 10% at Q1-end 2020.

Source: YRCW's Q2 2020 SEC 10-Q filing

Shortly after the CARES Act loan announcement, the company quietly filed another 8-K with the SEC in which they announced the covenant on their 0 million term loan with Apollo Global had been amended for a second time in 2020. Though it may not have seemed like much of a catalyst, the amendment completely lowered all near-term hurdles for the company and in turn, likely eliminated any serious investment risks through FY 2024. The amendment restored the original interest rate arrangement, allowed for a 100 basis point reduction on interest paid in cash, and lowered the minimum EBITDA requirement to 0 million through December 31, 2021.

Though the EBITDA covenant requirement steps back up to 0 million on March 31, 2022, the timeline and relatively low liquidity requirement of 5 million means company management can focus completely on executing their multi-point turnaround strategy. Centaur Investments believes that as the economic outlook improves and business operations see sequential quarterly improvement, the market will gradually lower the discount rate on the business’s equity. In Layman’s terms, this means sustained upward stock price momentum.

ELEVEN: The two low interest CARES Act loans totaling 0 million substantially reduce the company’s cost of capital while accelerating their fleet replenishment program and technology deployment.

An overwhelmingly important component of the list of catalyst drivers is the CARES Act loan which the Treasury Department announced on July 1, 2020. The first tranche of 0 million steers the company back on path towards profit improvement, by covering all deferred expenses linked to the pandemic. The second tranche of 0 million covers their annual CapEx budget of 0 to 0 million.

As explained in thesis point four, YRCW normally supports their CapEx budget through a combination of cash and high-interest bearing equipment leases, with roughly half of CapEx spending going towards fleet replenishment. The other half funds technology investment in hardware such as dock tablets, and cloud-based transportation management software. Because the company's old fleet is their Achilles heel, the budget constraint led to slow progress on fleet replenishment.

So, what makes the CARES Act loan such a game changer for the business is that the full 0 million is specifically for buying new tractors and trailers. The low interest on the loan enables the company to cut back high-interest bearing equipment leases in addition to the benefits from lower maintenance expenses. Altogether, this dramatically reduces the timeline for returning to profitability and it lowers the overall investment risk.

TWELVE: The 29.6% U.S. government stake tacitly pressures management to improve operational performance in a timely manner, likely accelerating the timeline to sustainable profitability.

The U.S. auto industry's progress since the great recession may serve as an example of the positive effects that come with government ownership of a publicly traded business. Centaur Investments studied Ally Financial (NYSE:ALLY), General Motors (NYSE:GM), and Fiat Chrysler (NYSE:FCAU) to evaluate whether those businesses improved after securing TARP funding.

Our assessment concluded that operations, profitability, and long-term focus improved substantially after those companies received TARP bailouts. For example, GM turned their Chevrolet Volt EV concept into a production model and is now a leading contender in the race to electrification and autonomous transport. Chrysler, on the other hand, focused on improving quality and building high-margin performance vehicles. Chrysler's strategy was so successful, it contributed to the improvement in European brands like Alfa Romeo and Maserati. Ally Financial became a leading consumer finance powerhouse, and eventually secured investment-grade credit ratings from S&P and Fitch.

In our view, congressional and taxpayer scrutiny pressured executive leadership at each company. The public scrutiny heightened management's incentives to strengthen their business and that maximized shareholder returns. Since the government sold off its stake in each company, all three have demonstrated financial discipline, strong profitability, and much improved product and service quality. GM's resilience after facing a massive production outage due to a labor dispute with the United Auto Workers last year, serves as supporting evidence of these observations.

Because YRCW currently faces similar pressures to what the automakers experienced, the phenomenal changes observed in GM, FCAU, and ALLY may certainly be replicated at YRCW. If and when these changes become apparent, new investors will be attracted to the shares and that should power further stock price appreciation.

THIRTEEN: Proposed 'Employee Stock Ownership Plan' may create a share price floor, reduce share price volatility, and empower employee engagement.

As a case in point to thesis item twelve discussed above, the U.S. Treasury Secretary has already demonstrated one way the government stake helps the business. Last month, Steven Mnuchin sent out a late night Tweet disclosing some details of a phone conversation he had with Darren Hawkins, YRCW's CEO.

Had a productive conversation with @JobsAtYRCW CEO Darren Hawkins. I am pleased that The YRCW board plans to discuss creating an Employee Stock Ownership Plan so that employees can voluntarily participate in the company’s revitalization and help shape its future.

— Steven Mnuchin (@stevenmnuchin1) July 14, 2020

Apparently, the company's board of directors is considering introducing an employee stock ownership program. Surprisingly, YRCW does not have an ESOP in place for employees to take ownership in the business. The implementation of such a program could put a floor on the stock price and help reduce volatility by repelling speculative day traders. ESOP demand may also drive upward share price momentum through increased investor bidding as the supply of available shares in the open market declines.

There are other indirect benefits as well, for example, the positive impact equity ownership has had on Starbucks' (NASDAQ:SBUX) corporate culture is a well-documented phenomenon. As a more directly comparable example, YRC's unionized LTL competitor ArcBest has had an ESOP in place for years, and the positive effect that program has had on the company's unionized workforce and share price performance is indisputable.

Increased employee stock ownership may help deliver cultural change at YRCW, as employees tend to become more engaged when they directly benefit from share price appreciation. An ESOP may also help recruit and retain experienced workers. Lastly, as new employees see others benefit from share price appreciation, they will be motivated to take part in the program as well, driving a positive feedback loop for all stakeholders involved.

FOURTEEN: Potential interest and amortization savings from deleveraging and replacement of high-interest equipment leases with lower-rate leasing and purchase options.

The price target of mentioned in the introduction was derived through a discounted cash flow analysis which factored in extremely conservative growth rates and did not account for a lower cost of capital. Some investors may not realize that the CARES Act loan actually lowers the company’s overall weighted average cost of debt from nearly 12% to 8.1%. The incremental returns on capital investments should free up substantial free cash flow to deleverage. A key area where the business can focus deleveraging efforts on is high-interest equipment leases, as mentioned earlier in thesis item number four.

Per the new capital structure and company SEC filings, we believe the CARES Act loan will allow the business to obtain new equipment leases on much more favorable terms. As the capital structure table below shows, for every 100-basis point decline in the effective interest rate on equipment leases, the weighted average cost of debt declines by 14 basis points. The table calculates several examples. The first calculation shows that lowering the 16.6% effective rate to 8.3% would lower overall WACD by 120 basis points. That translates to an interest expense decline of .8 million per year, from the projected total annual interest expenses including the CARES Act.

Source: Centaur Investments

Source: Centaur Investments

A second calculation shows that if the company were to eliminate equipment leases altogether, that would lower WACD by nearly 140 basis points from 8.1% to just 6.7%. That decline translates to a total interest expense decline of million per year. The company can accomplish this by simply purchasing new fleet equipment with the proceeds from Tranche B of the CARES Act loan, and all future equipment with excess cash flows freed up by the upgraded fleet itself, and other synergies from the multi-year strategy. These basic calculations demonstrate exactly why the CARES Act loan is a game changer for the company, and a boon to U.S. taxpayers’ new stake in the business.

Prospective investors should take these scenarios into account when evaluating the company’s overall debt balance and interest expenses in their mental or quantitative models, instead of categorically writing it off as a zombie company. The valuation model which will be shared later in this article does not speculate on how management will address the leverage situation, but still arrives at a valuation much higher than the current market capitalization. Lastly, considering James Pierson’s track record managing YRC’s books, it’s safe to assume he will make optimal decisions when it comes to capital allocation.

FIFTEEN: Removal of going concern uncertainty will renew customer interest, deliver sales growth, and allow company to continue defending market share.

The last item on the long thesis list is the simple notion that YRCW’s competitors have officially run out of rumors and stories to entertain YRCW’s customers with, as they try and win new business. On July 1, 2020, any former customers woke up to a whole new perspective of YRCW’s executive management’s capabilities. They also had an entirely new take on the ethics and business practices of the salesman that convinced them to leave YRCW.

The announcement of the 0 million CARES Act loan shook the industry and upset a lot of longtime YRCW haters. Looking ahead, the open runway for the company makes the future seem simple to predict. As operations improve, service quality will improve, the company’s culture will improve, and all these changes will drive more customers to do business with YRCW than ever before.

Going back to the central theme of this long thesis, YRCW’s size, scale, and network coverage in absolute terms, means it has far more opportunity to unlock existing value than any one of its LTL competitors. As you think about each of these 15 arguments, consider that the most efficient LTL carrier based on operating ratio currently trades for nearly 38x earnings and 5.7x its annual sales. The most directly comparable unionized LTL carrier, ArcBest, trades for nearly 30x earnings and 0.3x annual sales. YRCW, on the other hand, barely trades for a nickel per dollar in sales.

At these valuations, YRCW is in the best position to reward investors with outsized returns due to its suppressed market valuation relative to its actual size. Conversely, the rest of the LTL peer group has almost no room for operational improvement and forward growth seems fully priced in. This means the other carriers in this industry are likely better positioned to disappoint shareholders than they are to sustain outsized share price performance.

Think of this thesis as you would a formula one racing championship, where every nut and bolt, every team member, and every race helps rack up enough points to move up in ranking. In Centaur's view, the combination of each one of the thesis points detailed in this article will lead to considerable operating ratio improvement and ultimately sustainable profitability. If all works well, the company will eventually be in a position to where they have enough margin room to absorb short-term events like bad weather or a slower than typical LTL cycle, yielding positive full-year net income each year beyond FY 2022.

Centaur's Intrinsic Equity Valuation Assessment

In this section, all the arguments presented throughout this entire article will be condensed into a simplified financial model. We continue to believe that a discounted cash flow model approach to valuation is the best way to value the firm’s equity due to the company’s unique situation. Price-to-earnings and other multiple are not reasonably applicable due to the company’s negative earnings and the industry’s lofty valuations. Nevertheless, a basic multiple analysis is also included in this section.

In this latest iteration of the financial model presented in all prior articles, substantial revisions have been made. In addition to complete data for FY 2019 and 6 months' worth of financial data for FY 2020, a substantial decline in total revenue, net income, and free cash outflows are now projected for FY 2020 and FY 2021. These changes were deemed necessary to properly reflect the company’s current situation and new risks relative to last year.

The model assumes sales growth will return in 2021, but the 4 to 6 quarters in lag between new equipment orders and actual delivery will delay return to profitability. Additionally, the sizeable capital investments and working capital commitments are expected to weight on free cash flow in FY 2021.

Beyond 2021, the ramp up in fleet replenishment, higher load factor, growth into capital structure, and lower cost of capital are forecast to contribute meaningfully to net income and free cash flow. Lastly, the model has CapEx and working capital stabilizing beyond 2022, as the fleet age catches up to the industry average, and the company’s software migration to the cloud is complete.

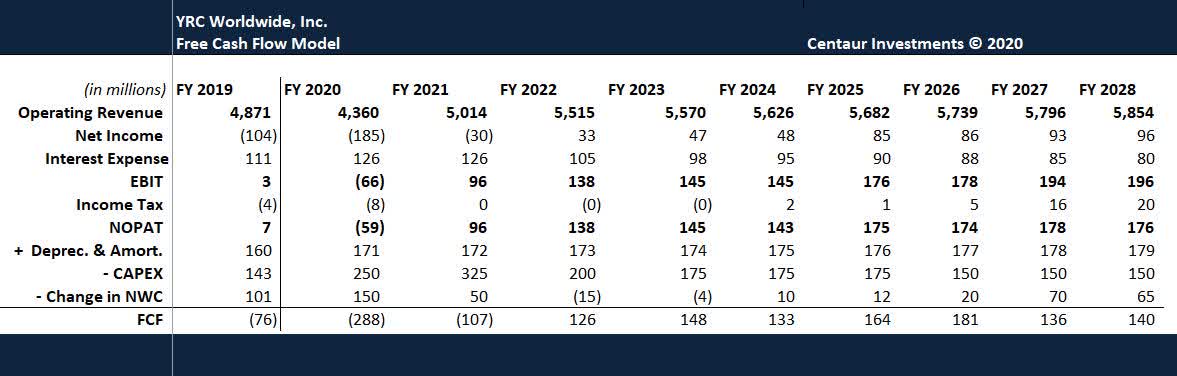

The table below shows Centaur Investments’ projections for free cash flow as applied in a 10-year horizon discounted cash flow valuation model.

YRCW - Free Cash Flow Model

Source: Centaur Investments

Source: Centaur Investments

The process of arriving at the free cash flow model pictured above, started with review of well over 10 years of annual and quarterly financial data for YRCW. Assumptions were drawn from the yearly and quarterly changes in each line item, as well as feedback shared by company management during conference calls and presentations. These assumptions were used to project financial performance 10 years into the future. After that, several iterations of the model were produced before arriving at the most conservative and rational one presented here.

Prospective investors are encouraged to model out the company’s financial statements to the same 10-year horizon period, to assess for themselves the gigantic effect on operating income each 100-basis point decline in the company’s operating ratio will have. The positive effect on net income and free cash flow caused by getting the OR down to reasonable levels such as 95% to 93%, is quite remarkable and is something investors need to see for themselves. For pragmatic purposes, the model observed here keeps the company’s operating ratio above 96% through year 10.

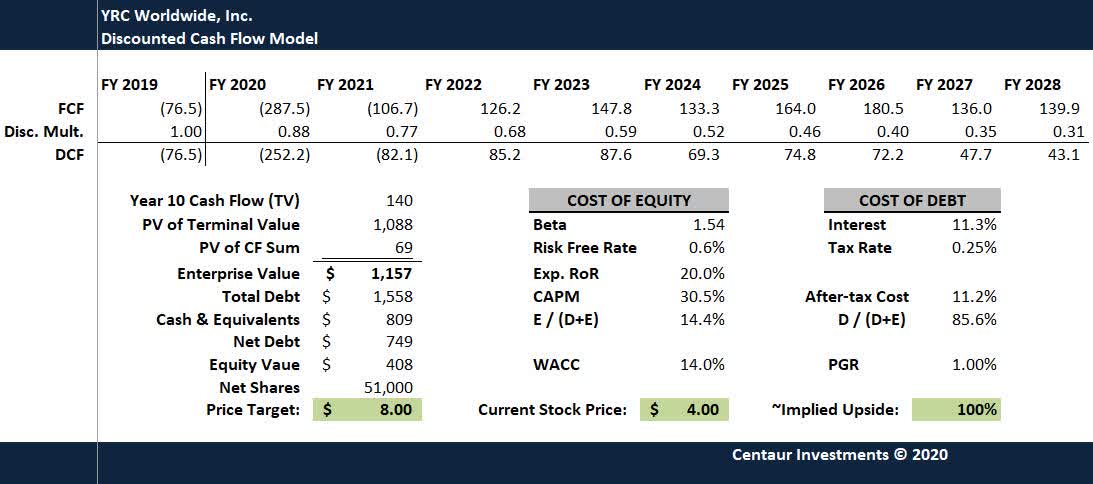

YRCW - Discounted Cash Flow Model

The discounted cash flow model below included substantial revisions to the company’s capital structure. Although the new CARES Act loan dramatically lowers overall cost of debt, that new cost of debt calculation is not reflected in the model due to the uncertain outcome of the Congressional Oversight Committee scrutiny of the loan terms.

Centaur Investments believes that any interference in the loan terms would be detrimental to all stakeholders, including the thousands of middle-aged rank-and-file workers who have dedicated decades of their lives to YRCW companies. As these hard-working Americans anxiously await retirement, the quality of their livelihoods at retirement depends on this company’s survival. For them, there is no starting over, even if the industry could absorb YRCW's customers without service disruptions. Seeing things from this perspective, makes the creative destruction some investors wish for seem unfair and perhaps outright inhumane.

Any attempts by the Oversight Committee to alter the rates on the two CARES Act loans would adversely affect the company’s ability to service its debt, and dramatically reduce the probability of realizing the high investment returns projected in this thesis. Due to this reasoning, it seems reasonably improbable that the Oversight Committee will attempt to alter the terms of the two CARES Act loans.

Nevertheless, that risk has been embedded in the DCF model in two ways. First, the expected market return has been increased from 11% to 20%, to reflect opportunity costs and inherent risks. Secondly, the company’s overall cost of debt was reduced by 100 basis 11.3%, instead of the 420-basis point reduction which the CARES Act loans call for. The cost of debt will be lowered again when it can be confirmed with absolute certainty that the terms of CARES Act loan will not be altered.

Source: Centaur Investments

Source: Centaur Investments

As the DCF valuation above shows, this latest assessment of the business concludes that the company’s equity should be valued closer to 8 million. Factoring in the U.S. Treasury Department’s newly issued shares, the valuation yields a price target , compared to the suggested a year ago. This implies the shares still have near term upside opportunity of 100% from the quoted at market close on August 12, 2020.

Even though the company’s second quarter earnings surprised to the upside, investors should expect to see third quarter results impacted by expenses deferred or accrued during the second quarter. With the company having recalled most of its workforce previously on furlough or layoff status, operating expenses are trending higher in the third quarter. The deferrals, accruals, and paid-in-kind interest charges from the second quarter combined with normalized operating expenses in the third quarter may lead to a larger than expected earnings loss. Therefore, investors should not be surprised to see the shares trade flat or decline after Q3 earnings are reported.

However, If YRCW’s Q3 financial performance is better than expected or there is a market-moving catalyst such as a vaccine, the shares may start trekking toward double-digits by the end of the year. All else equal, Centaur's price target for the shares stands firm at . This is a considerably cheap valuation, considering all the information presented throughout this article, as well as YRC's ample liquidity, hidden real estate value, low risk of covenant breach, and no expected loan repayments until 2024.

YRCW - Industry Multiple Analysis

Even though the market remains resilient despite an ongoing pandemic, investors must recognize that the we are experiencing a period of extreme uncertainty. In addition to the pandemic, the economic recovery hinges on congress's ability to pass a second stimulus package in a timely manner. Additionally, with a major presidential election coming up in the U.S., there is little ability to predict how the market will behave as we approach November.

The transportation industry data shared early in the article shows that despite the reopening of the economy, freight volumes and overall business activity remain subdued. In spite of these realities, the stock price multiples for transportation companies prove that the market is no longer pricing in the period of supply-demand destruction from the second quarter of the year.

On the contrary, investors are increasingly betting on a v-shaped economic recovery. For added perspective, transportation industry multiples and other relevant data necessary to cross-compare transportation companies are presented in the image below.

YRCW's Industry Comps

Source: Seeking Alpha, Centaur Investments

Source: Seeking Alpha, Centaur Investments

0

0

0

0

0

0